Home Loan Eligibility for a Flat in Vadodara: How Much Can You Borrow in 2026?

Read the full blog and check your eligibility

📍 Vadodara, Gujarat 🗓 June 2026 ⏱ 7 min read

If you are planning to buy a flat in Vadodara, one of the first questions you will face is: how much home loan am I actually eligible for? The answer depends on several factors including your income, existing liabilities, age, credit score, and the property value. In this guide, we break down exactly how lenders calculate your eligibility so you can walk into a bank with a clear number in mind.

How Do Banks Calculate Home Loan Eligibility?

Banks and housing finance companies in India use a simple rule to determine how much you can borrow: your total EMI obligations including the new home loan should not exceed 40 to 50% of your monthly income. This ratio is called the Fixed Obligation to Income Ratio (FOIR).

For example, if your monthly take-home salary is Rs. 80,000 and you have no existing loans, a lender may approve an EMI of up to Rs. 36,000 to Rs. 40,000 per month. At current home loan interest rates of around 8.5% to 9% for a 20-year tenure, that translates to a loan amount of approximately Rs. 38 lakh to Rs. 42 lakh.

Beyond FOIR, lenders also evaluate your credit score (a CIBIL score of 750 or above gives you the best rates), your employment stability (salaried vs self-employed), your age (younger borrowers get longer tenures), and the property's legal status.

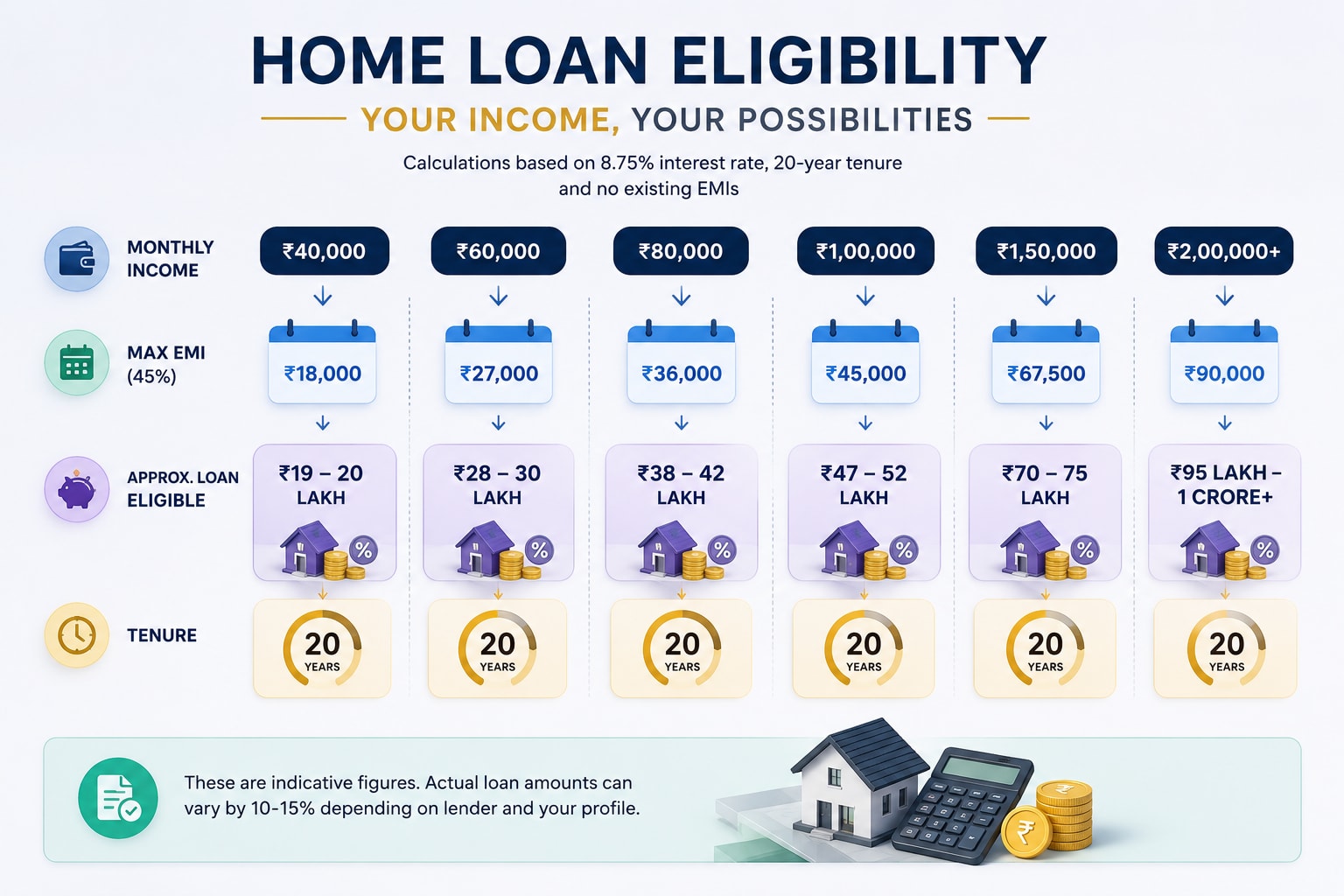

Home Loan Eligibility by Income: Quick Reference for Vadodara Buyers

The chart below gives you a rough estimate of loan eligibility at an 8.75% interest rate, 20-year tenure, and no existing EMIs:

These are indicative figures. The actual amount sanctioned can vary by 10 to 15% depending on the lender and your profile. If you are self-employed, most banks apply stricter FOIR norms, typically 40% instead of 50%.

To match this against what properties are actually available in Vadodara at these price points, browse the verified property listings on Kuber Property filtered by budget and locality.

How Much Does a Flat in Vadodara Actually Cost?

Understanding your eligibility makes more sense when you compare it against real property prices in Vadodara. Here is where the market stands in 2026:

- 2 BHK flats in Gotri and Waghodia Road: Rs. 45 lakh to Rs. 75 lakh depending on size and project

- 2 BHK flats in Alkapuri and Akota: Rs. 60 lakh to Rs. 1.1 crore, premium for central location

- 3 BHK flats across Vadodara: Rs. 70 lakh to Rs. 1.5 crore depending on locality and amenities

- 1 BHK flats in emerging areas: Rs. 25 lakh to Rs. 40 lakh, the fastest growing segment in 2026

This means a buyer earning Rs. 80,000 per month can realistically target a 2 BHK in Gotri or Waghodia Road with a standard 80% loan-to-value arrangement, putting 20% as down payment and financing the rest. If you are exploring Waghodia Road specifically, the Waghodia Road area guide covers current pricing and upcoming projects in detail.

Key Factors That Can Increase Your Home Loan Eligibility

If the eligibility amount you calculated is lower than what you need, here are practical ways to improve it before applying:

1. Add a co-applicant

Adding a working spouse or parent as a co-borrower combines both incomes for eligibility calculation. This is the single most effective way to increase the loan amount, in some cases by 40 to 60%.

2. Clear existing loans before applying

Every existing EMI reduces the amount a bank will lend you. Paying off a car loan or personal loan before applying can significantly improve your eligibility. Even reducing outstanding credit card debt improves your FOIR ratio.

3. Opt for a longer tenure

Extending your loan tenure from 15 years to 25 years reduces the monthly EMI, which allows you to qualify for a larger loan. The trade-off is higher total interest paid, but it gives you the flexibility to prepay when income grows.

4. Improve your CIBIL score

A score below 700 can result in rejection or significantly higher interest rates. Pay all EMIs and credit card dues on time for six to twelve months before applying. Avoid multiple loan enquiries in a short period as each hard enquiry slightly dips your score.

Pro tip: Always get a pre-approval letter from your bank before shortlisting properties. It confirms your budget, speeds up the transaction, and gives you negotiating credibility with sellers.

Which Banks Offer Home Loans in Vadodara?

Most major national and regional lenders are active in the Vadodara market. Here are the primary options buyers use:

- SBI Home Loans - typically the lowest rates for salaried applicants with clean credit

- HDFC Bank and HDFC Ltd - fast processing, widely used for new project purchases

- ICICI Bank - strong digital process, good for self-employed borrowers

- Bank of Baroda - headquartered in Vadodara, familiar with local property documentation

- LIC Housing Finance - preferred by conservative borrowers with longer tenures available

Interest rates as of mid-2026 range from 8.5% to 9.5% for most salaried borrowers. A 0.25% difference in rate on a Rs. 50 lakh loan over 20 years is a difference of nearly Rs. 1.8 lakh in total interest, so comparing at least three lenders before committing is worth the effort.

If you are considering flats in Alkapuri, one of Vadodara's most sought-after localities, explore the Alkapuri property guide to understand what your budget can realistically get you in that area.

What Costs to Budget for Beyond the Loan

Home loan eligibility tells you how much you can borrow but your total outflow on a property purchase is higher. Here are the additional costs to plan for:

- Down payment: Minimum 20% of property value (banks fund up to 80% LTV)

- Stamp duty in Gujarat: 4.9% of property value (check current rates as these are revised periodically)

- Registration charges: 1% of property value, capped at Rs. 30,000

- GST: 5% applicable on under-construction properties, nil for ready-to-move

- Brokerage: Typically 1 to 2% if using an agent

- Home loan processing fee: 0.25% to 1% of loan amount

On a Rs. 60 lakh property, your all-in cost including stamp duty, registration, and GST (if under construction) can add Rs. 5 to Rs. 7 lakh over the property price. Budget for this before finalising your purchase.

Final Checklist Before Applying for a Home Loan

- ✅ CIBIL score above 750 (check free at CIBIL or BankBazaar)

- ✅ No more than 2 to 3 existing EMIs, pay off smaller ones first

- ✅ Salary slips or ITR for the last 2 to 3 years ready

- ✅ Property documents verified: title deed, RERA registration, encumbrance certificate

- ✅ Down payment amount available in liquid savings, not locked in FD or investments

- ✅ Pre-approval letter obtained before making an offer on any property

Once you have a clear picture of your eligibility and budget, the next step is finding a property whose legal documentation is clean and lender-approved. Browse verified listings on Kuber Property across Gotri, Alkapuri, Waghodia Road, Akota and Manjalpur with complete documentation support to make your loan application smoother.

Ready to Find Your Home in Vadodara?

Know Your Budget. Find the Right Flat. Move in Sooner.

Explore verified 2 BHK and 3 BHK flats across Gotri, Alkapuri, Waghodia Road, and Akota. Every listing on Kuber Property comes with complete documentation support, so your home loan gets approved faster.

Browse Properties NowOr call us directly to speak with a property expert in Vadodara

Get in Touch with Kuber Property